OT - WSJ article on Hackett, not flattering

Link - https://www.wsj.com/articles/fords-new-ceo-has-a-cerebral-styleand-to-many-its-baffling-1534255714

"Senior executives at Ford Motor Co. F 0.42% have come to expect emails from their new boss, Chief Executive Jim Hackett, that include links to TED Talks and articles from Science Daily. They often come around 11 p.m., when he catches up on his reading.

The former chief of an office-furniture maker, Mr. Hackett frequently references the work of theoretical physicist Geoffrey West and uses terms such as “think phase” (a concept from his design background) and “clock speed” (a phrase from computing). In conversations, he often reaches for the nearest piece of paper or whiteboard to articulate his thinking by sketching out a diagram."

As someone who has ten years of experience in the automotive industry, you understands the importance of manufacturing (this is why Toyota makes so much money) competitiveness, and the importance of high margin product.

Although Hackett hasn't been at Ford for very long, these quotes don't inspire confidence. I don't see the focus on product or manufacturing like Marchionne had during his tenure at FCA.

And the 28 year old Chief of Staff is weird.

August 15th, 2018 at 8:55 AM ^

Harbaugh

August 15th, 2018 at 10:29 AM ^

Seriously.

How the hell do you read this, think to yourself, "I'm going to post this on the MGoBoard" and during the time between not stop yourself?

August 15th, 2018 at 9:00 AM ^

I'm not going to "subscribe" just to read a single article but I don't see from what you've quoted anything unflattering. Quirky, eccentric; certainly. Weird; maybe. The guy clearly knows how to get shit done though.

August 15th, 2018 at 9:05 AM ^

He's using nonsense words because he has no idea what he's talking as it pertains to automotive manufacturing.

August 15th, 2018 at 9:20 AM ^

As an engineer, this article makes me like Hackett even more than I already did.

The fact that Wall Street investment types don't seem to grok him is just icing on the cake. :)

August 15th, 2018 at 9:26 AM ^

Had to look up the work grok. Plus 1 to you, if I could vote.

August 15th, 2018 at 9:31 AM ^

Congrats, Ford stock is the same price today as it was in 1989. Even with the dividend, it's massively underperformed the S&P500 during the same 30 year period.

With inflation, it's even worse.

August 15th, 2018 at 9:39 AM ^

Why are you piling on a former AD, who did good things at Michigan. Are you Chevy Guy or trolling?

August 15th, 2018 at 10:38 AM ^

there are lots of disturbing images of cartoon children peeing on car symbols. Not sure why, but it seems weird that it is usually American car companies being peed upon.

August 15th, 2018 at 10:55 AM ^

I always wondered why Bill Watterson never sued the shit out someone for appropriating his creation (Calvin), especially when he never in a million years would think this is remotely funny.

August 15th, 2018 at 11:06 AM ^

Watterson is a fascinating character. He's media-averse, believes in artistic purity over commercialization, and he's never licensed Calvin & Hobbes to sell anything (I believe there was one tiny exception a long time ago for some charity event, but nothing mass market). Literally everything you see out there using the Calvin & Hobbes likeness is unlicensed-- he's just not super litigious. Which is another reason he's one of the most unusual Americans ever.

August 15th, 2018 at 2:14 PM ^

The publishers, not Watterson, are typically the ones who send these out.

August 15th, 2018 at 3:49 PM ^

As he should. You don’t appropriate another’s work without their permission.

August 15th, 2018 at 9:41 AM ^

And Hackett has been there for how much of that time, exactly?

August 15th, 2018 at 9:41 AM ^

Good thing I bought Ford Stock in the spring of 2009! ;-)

August 15th, 2018 at 9:41 AM ^

Reading your comments, I'm pretty sure that you had a preconceived opinion of Ford and Hackett. This article doesn't reflect negatively on the man unless you want it to.

I'm sorry that you lost money on Ford stock, or were laid off, or Ford stopped buying from your company, or whatever happened. Hell, I lost money on Ford stock too.

But aside from your obvious bias, there's a deeper issue here: if you need every stock to match the S&P 500...just buy an S&P 500 ETF. It's a smart idea already!

August 15th, 2018 at 12:19 PM ^

Agree and agree.

None of the quotes make me think poorly of Hackett. It's just his style. Seems like a preconceived opinion from the OP.

And buy the ETF.

August 15th, 2018 at 9:54 AM ^

Q to karpodiem: What was Ford stock price when the real estate-driven investment bubble burst in 2008? Why did you pick 1989 as the basis for your comparison?

August 15th, 2018 at 10:03 AM ^

Accoriding to this:

https://www.stocksplithistory.com/ford-motor/

Ford stock has split 4 times since 1989, meaning you'd have 5.48x as many stocks now as you would have had in 1989. That seems to account for 5.8% gains per year. You'd have to look at where you'd be at with reinvested dividends, but I'm guessing it's significantly higher than that. Historically, they've been in the 3-6% range. That's still not going to match the S&P 500, but no one really expects an established auto manufacturer distributing dividends to compete with the tech companies currently driving the growth of the S&P.

August 15th, 2018 at 10:40 AM ^

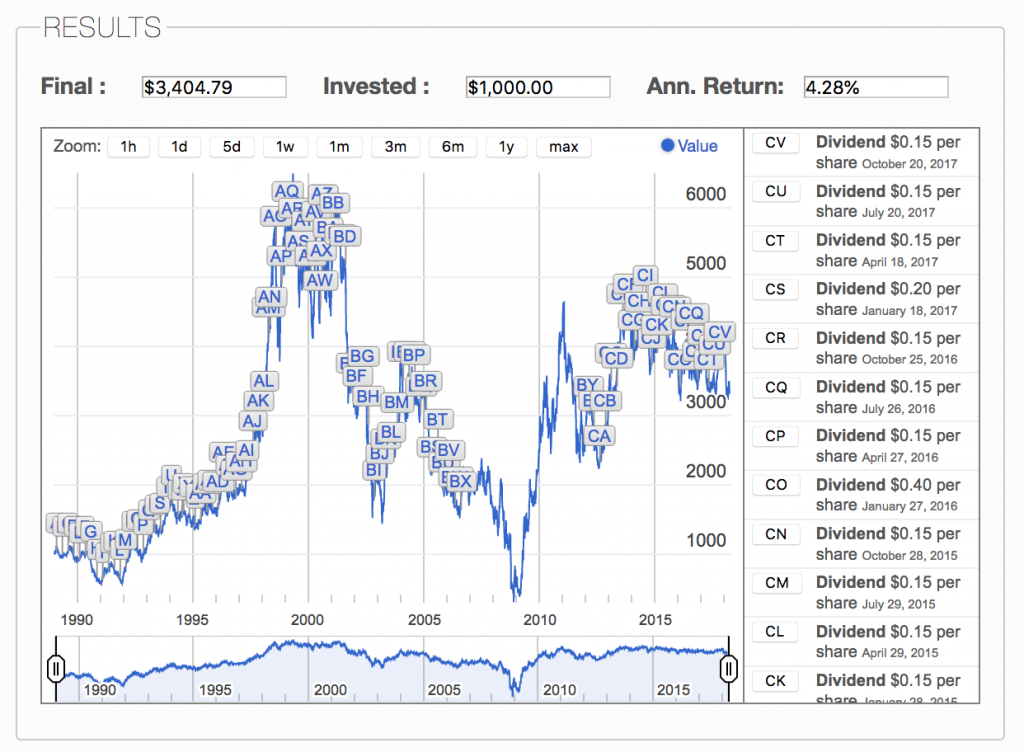

I don't really have a dog in this fight, but data is available to settle this question. If you put $1,000 in Ford stock on Jan. 1, 1989, and reinvested all dividends since then, your investment would be worth $3,404.79 today (including stock splits), according to dqydj.com.

An annual return of 4.28% is … not especially great for a stock investment. You'd like to see it around 6% or 7%.

August 15th, 2018 at 12:58 PM ^

Does that take into account the splits? I think I tried using that and couldn't figure out how, by adding dividends in, you'd have a lower return than just the splits. Based on their normal yield, of 3-5% that I saw, that seems to be about what you'd expect to see without taking into account splits. If it's not taking splits into account, then total return is somewhere around 10%, which is about what I'd expect.

August 15th, 2018 at 3:39 PM ^

So, like, five things:

First: Take what I say with a grain of salt. I do this as a hobby/retirement investor, not for a living or even to supplement my income.

Second: Here's the full link to the DQYDJ calculator I was using: Stock Return Calculator with Dividend Reinvestment (DRIP) for EVERY Stock.

Third: You might follow that link and observe the big red notice at the top saying they lost their API and include no stock data since March. If so, you're doing better than I did. That seems like an important caveat, tho' less so since we're talking about a nearly 30-year investment.

Fourth: DQYDJ does claim to account for stock splits:

Here is a stock return calculator which automatically calculates dividend reinvestment (DRIP). It has daily resolution and properly accounts for stock splits and special dividends.

and

The calculator internally creates a datastructure which contains the initial purchase and the price fluctuations using stock closing prices on each day. (Normal) splits and dividend events cause us to increase the modeled number of shares held. Reverse splits will reduce the number of shares held.

However:

The stock total return calculated is idealized, based on closing prices, and will not match the exact returns. We are not modeling taxes, management fees, dividend payment timing, slippage, or other sources of error. It is possible that the dataset contains errors as well.

Fifth: The 4.28% calculated is an annual return, which accounts for compounding and isn't going to give you the same number as just multiplying out the number of shares owned after 30 years of stock splits.

But regardless of all this, the takeaway is roughly the same: Saying a stock's price is the same now as it was in 1989 doesn't mean an investment hasn't gained in value, clearly. Also, it isn't a useful way to compare how a company's performed in that span.

But if your context is that you're picking any stock you'd like to have put your money in 30 years ago, Ford's return has been below what you'd like to see. By comparison, if you'd put your money instead in a mutual fund tracking the S&P 500 in 1989 and reinvested all dividends — and assumed no fees, no added costs, yada yada yada — you'd have seen an annual return of 10.363% without adjusting for inflation.

On the other hand, Ford might look pretty good compared to the rest of the industry. GM stock's annual return since 1989, for example, is about 2.40% using the same calculator.

August 15th, 2018 at 10:21 AM ^

Which is considerably better than GM and Chrysler faired over the same time period.

DOH!

August 15th, 2018 at 2:23 PM ^

But $F is one of the best short-selling stocks I've experienced. Never drops below $9/share, always ranges $9-11/share. Back when I was playing with RobinHood, $F was what was keeping me in the black while gambling on pharmaceutical companies to make/break their FDA testing.

So, thanks Ford for that. Bailed me out when $MACK didn't get one of their drugs approved.

August 15th, 2018 at 9:34 AM ^

Why does he need to? Is he head of manufacturing?bimbsure Ford is paying somebody into the 7 figures to make sure worldwide manufacturing runs smoothly.

August 15th, 2018 at 12:12 PM ^

"bimbsure Ford is paying somebody into the 7 figures..."

Which of the Fords named one of their children "bimbsure?"

August 15th, 2018 at 11:00 AM ^

I agree. Time will tell if he can transform Ford.

August 15th, 2018 at 11:43 AM ^

"Karpodiem" ? Must be the expert on nonsense words

August 15th, 2018 at 1:09 PM ^

karpodiem... you understand you are not as smart as you think you are, right? what a total waste of time to post something like this for no reason other than to prove..... what??????.

August 15th, 2018 at 1:47 PM ^

Never before seen:

Manufacturing Arrogance.

August 15th, 2018 at 5:05 PM ^

His job isn't to understand automotive manufacturing. To be frank, given Ford's performance over the last 30 years perhaps it's best that if he doesn't...

August 16th, 2018 at 1:36 AM ^

Hacket isn't the one in this thread that doesn't know what he's talking about

August 16th, 2018 at 11:26 AM ^

"He has no idea what he's talking (sic) as it pertains to automotive manufacturing."

That's also not his job. Rather, it is to set a direction for the company and to be accountable for the outcome.

As I recall, Alan Mulally didn't know about automotive manufacturing, either. He was President of Boeing Commercial Airplanes before becoming CEO at Ford. He did, (and Hackett does) understand complex assembly, operations, supply chain, design, marketing, sales, finance, etc. Each is highly transferable across industries.

Your "you don't know automotive" attitude is exactly what I have observed in many with whom I've worked over the years in the industry. It's a close relative of "Not Invented Here," and it leads to stagnation and group-think. Which may also, come to think of it, explain Ford's putrid share price performance over the past several decades.

August 15th, 2018 at 9:51 AM ^

An easy way to get behind the WSJ paywall is to Google search for the article title. The first WSJ should let you view the entire article.

August 15th, 2018 at 10:18 AM ^

You can often read full WSJ articles by searching for a link on Facebook or Twitter, too — like this:

Inside Ford's bumpy turnaround: Some executives use the CEO's 28-year-old chief of staff to translate the boss's intentions. https://t.co/cCqZQ8nkdo

— The Wall Street Journal (@WSJ) August 14, 2018

August 15th, 2018 at 2:17 PM ^

Here is a link to an unblocked reprint of the article.

August 15th, 2018 at 9:01 AM ^

This is the man who landed the white whale, James Joseph Harbaugh. How is he expected to be able to interact at an intellectual level of mere mortals?

August 15th, 2018 at 9:01 AM ^

We'll take him back if Ford doesn't want him anymore.

August 15th, 2018 at 9:03 AM ^

So.....Patterson is still leading for the starting QB slot?

August 15th, 2018 at 9:53 AM ^

Actually no.

I have it on good word from this guy on counterstrike that Michigan will start Rashan Gary at QB in South Bend. We will run lots of wildcat and triple run option with Higdon, Evans, and Mason in the backfield all at the same time with Gary.

As for Patterson, he is starting as a WR. We plan to utilize him a lot on end around plays where he has the option to keep the ball and run with his feet sweeping around the flank or to look downfield for a pass.

August 15th, 2018 at 10:11 AM ^

You laugh, but I'd love to see the LB's face when Gary trots out, call "Hike," and launches his 280 lbs at 4.6 speed in his direction. We may see a play crap himself on the field.

August 15th, 2018 at 10:18 AM ^

Not mention I read that Gary is going to give ND the arabian goggles, and one or two other things too...

August 15th, 2018 at 9:04 AM ^

You're comparing Hackett to Marchionne? I don't know, Hackett has been doing this for 2 - 3 yrs. Maybe slow your roll a little.

August 15th, 2018 at 9:06 AM ^

I just read the article. It didn’t come across as unflattering to me. It emphasized that he does things in a different way and the executives are still feeling him out and adjusting. There were several anecdotes in the article that reflect positively on him. For example, giving his reports more decision-making authority. Not sure why OP is so negative, unless that opinion is formed by more than just the article posted.

August 15th, 2018 at 9:08 AM ^

"Not sure why OP is so negative"

The stock price, floundering in China/South America, two door Bronco is DOA against new Wrangler, lack of upcoming competitive product based on what I know is in the supply chain pipe for the next two years.

August 15th, 2018 at 9:09 AM ^

Ok, so that opinion is formed by more than what is in the article.

So basically, you have a negative opinion of Hackett/Ford, and the article had certain themes that seemingly validated that opinion for you. Fair enough.

August 15th, 2018 at 9:38 AM ^

You’re basing it on the stock price? It has a >6% yield and ~5.5 P/E. Meanwhile, companies showing losses year in/year out are selling at far higher valuations. People can talk all they want about projected growth, but I’ll take the undervalued stock with actual earnings and a bunch of cash on hand. I may be way off base in my investing, but claiming Ford’s stock price is evidence of anything other than an undervalued company is crazy. As Keynes said, “the market can remain irrational longer than you can remain solvent,” and this market is nothing if not irrational.

August 15th, 2018 at 9:57 AM ^

These problems are due to the previous ousted CEO. Do you have any idea how long it takes to turn a company around. Especially an auto manufacturer given the long product lifecycles and deeply embedded culture.

August 15th, 2018 at 10:10 AM ^

not a single one of those things have anything at all to do with hackett. none.

maybe he'll bomb out, maybe not. i have no idea, but you don't either. this is just a puff piece on someone who thinks differently than what his colleagues have grown accustomed to. he won't fail or succeed based on whether or not he uses phrases like 'think phase' or 'clock speed.'